Insights from 3,000+ WXO experience professionals

To see what practitioners actually need, we analysed open‑ended responses from 3,000+ experience professionals in 50+ countries. When people apply to join the WXO, we ask two questions:

- What’s your biggest challenge today?

- What would most transform your world?

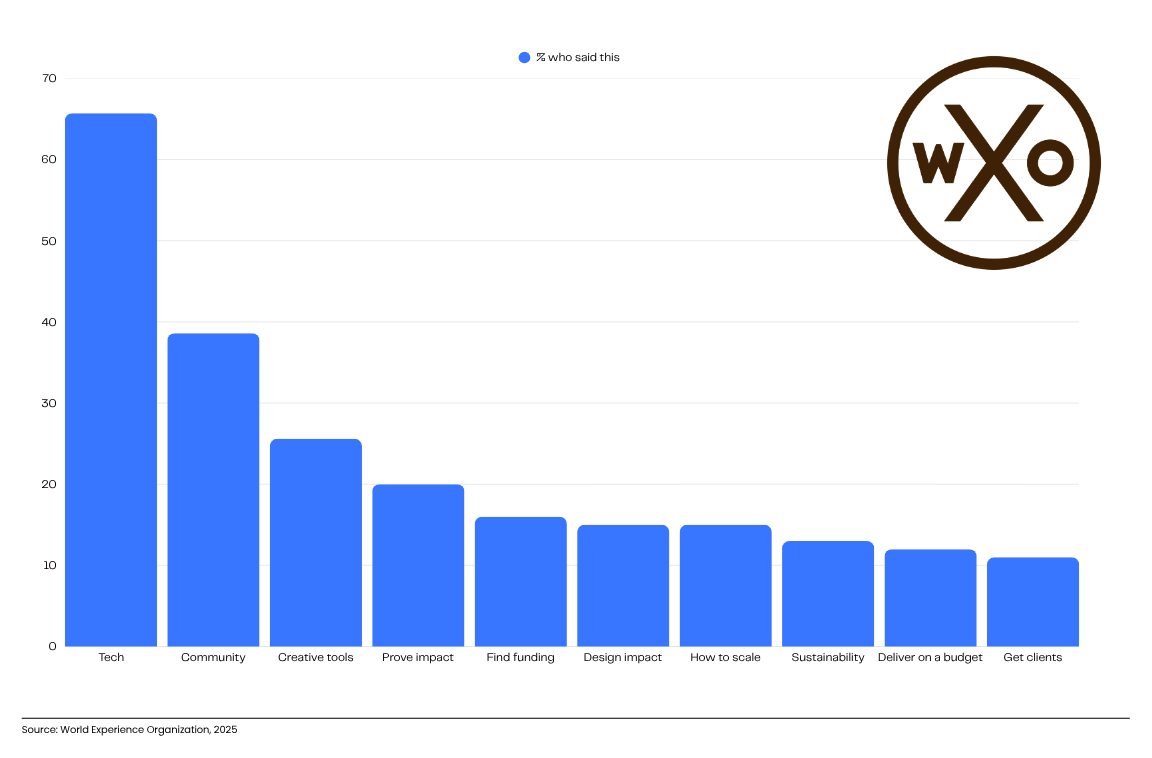

After analysing the responses using a mix of artificial and human intelligence*, ten principal challenges emerged:

- 65.7% – Tech (Spatial / AI / XR)

- 38.6% – Belonging & Community

- 25.6% – Creativity & Craft

- 20.0% – Prove It (ROI/ROX & Buy‑In)

- 16.3% – Funding & Investment

- 15.0% – Designing for Impact

- 14.7% – Scale‑up & Expansion

- 12.6% – Sustainability (Eco & Ops)

- 11.0% – Creativity Constrained by Budget

- 10.0% – Get Clients & Business

Source: WXO member applications, November 2025. Respondents could select multiple tags. Totals exceed 100%.

Each of the ten battles is brought to life here by verbatim quotes. This is what matters now – the real voices of the people who power the Experience Economy.

Technology: How to Harness Tech to Make Better Experiences (65.7% of respondents)

The strongest challenge our members face: using technology to deepen real‑world experiences, not distract from them. Whether working in museums or malls, on stages or in streets, practitioners are open to Spatial, AI and XR – but only when those tools earn their place in the creative journey.

Here are ten examples of what people told us:

- ‘Connecting digital and physical world experiences better.’

- ‘Enhancing physical environments with immersive digital interactions through innovative multimedia design.’

- How to seamlessly integrate physical and digital experiences.’

- ‘Designing experiences that authentically connect people across both digital and physical spaces.’

- ‘In the realm of phygital experiences, we focus on enhancing physical environments with immersive digital interactions through innovative multimedia design.’

- ‘The digital and real world are merging with the popularisation of VR (BALANCE!).’

- ‘How do you further engage people in physical spaces?’

- ‘How we can continue to bridge the gap between digital and physical worlds by creating unique experiences combining art and technology. And of course, AI!’

- ‘Make digital spaces feel as engaging and human as physical ones, and physical spaces as dynamic and interactive as digital.’

- ‘How do we properly implement mixed‑reality hardware integration?’

What this means – and what we do next

Our members want fewer showreels and more road‑tested examples: credible, repeatable examples where a tech stack has genuinely improved creativity, performance and scale. They want case studies with budgets, timelines, failure modes and outcomes – not just highlight reels. So they can take that technology back into their work, and create better experiences.

Community: Build Belonging, Not Just a Network (38.6% of respondents)

While the remote / hybrid ways of work that came out of the pandemic may have raised productivity in the short term, it left many creators in the Experience Economy working – and feeling – alone. In an industry that thrives on collaboration, and for animals that are hypersocial, this can affect business and wellbeing.

So it’s not surprising perhaps that experience professionals say they need a straightforward way to find trusted peers and collaborators they can build with. And just anyone won’t do. Whether they’re mentor or mentee, they want to be with a community of people who understand the Experience Economy.

Here are ten examples of what people told us:

- ‘Connect me with like‑minded professionals.’

- ‘Place me in the centre of an inspiring, like‑minded community. Endless possibilities, collaboration and support.’

- ‘Networking is everything… connect with industry colleagues and forge relationships with future partners, collaborators and friends.’

- ‘Help me find a group of colleagues, mentors and accountability partners to share ideas and techniques with.’

- ‘Connect with a community of like‑minded creators and innovators for inspiration, networking and cross‑pollination.’

- ‘Finding like‑minded people and belonging to a community of people as curious and passionate as I am.’

- ‘Access to a network of immersive professionals who want to solve the same problem.’

- ‘Connect me to other thought leaders and innovators in the experience world.’

- ‘Connect me with like‑minded folks, open opportunities to craft newer experiences.’

- ‘Outside of the company – I need to build my world more outside this company.’

What this means – and what we do next

Experience professionals prefer a place where people understand them, ideally curated groups with people who share common challenges. That’s where we’ll focus.

Creativity & Craft: Tools, Techniques, Standards, Learnings (25.6% of respondents)

Experience creators want a portable toolkit. They want frameworks, templates and examples that work across theatre, games, retail, culture and LBE. Many describe operating in an emerging field without shared standards or reliable benchmarks, where quality under constraint is the core skill. The challenge? A constant need to reinvent from scratch.

Here are ten examples of what people told us:

- ‘Teach me tools and techniques.’

- ‘Open a door to the best industry examples.’

- ”Exposure to the best and brightest designing jaw‑dropping, inspiring experiences that stretch us to deliver at a higher calibre.’

- ‘Knowledge on how to solidify my frameworks and praxis in designing immersive experiences.’

- ‘Learn from others’ successes and mistakes.’

- ‘Exposure to ideas, concepts and different ways of delivering.’

- ‘Creating experiences in a fractured media landscape.’

- ‘Exposure to the best experiences in the world.’

- ‘Provide greater access to and knowledge of what is happening out there – there’s so much, and no one great resource to dive into!’

- ‘The field is still emerging; fragmentation and lack of standards – everything is custom built.’

What this means – and what we do next

Our members want shared language and open resources – a living library of proven tools and evolving techniques. The WXO will continue collecting and publishing working frameworks, not fixed “best practices”, so creativity can scale without losing its spark.

Impact & How to Prove it: ROI, ROX & Buy‑In (20.0% of respondents)

Experience professionals no longer just want to make great experiences – they need to prove they work. Whether to clients, CFOs, sponsors or city funders, the evidence of impact is what converts stakeholders into advocates. The challenge isn’t enthusiasm, it’s translation: turning emotion, engagement and memory into metrics decision-makers trust. This is the evidence that unlocks budgets.

Here are ten examples of what people told us:

- ‘Help to find connective tissue with like‑minded experiential marketers and continue to reinforce the different types of ROI from experiential marketing.’

- ‘Most brands are uncertain about ROI for their investment in an immersive installation.’

- ‘I also want to track the qualitative ROI or ROE (return on experience) which is challenging.’

- ‘How to justify the ROI to show management.’

- ‘Getting clients to yes more often on immersive experiences – better quality ROX for them.’

- ‘How do you create buy‑in within a large organisation for experiences centred on community building, when the organisation has always prized content above all?’

- ‘Achieve buy‑in from governments and funders that investing in culturally and creatively rich visitor experiences drives physical, psychological and economic wellbeing.’

- ‘Measuring the emotional and brand impact is complex – yet vital for demonstrating value to stakeholders and clients.’

- ‘Our clients have not had the exposure. Having resources and examples to share with them is so important.’

- ‘I spend so much of my time trying to convince people that experience design is important and fighting for attendee journeys and emotional engagement.’

What this means – and what we do next

Evidence wins budgets. Members are asking for practical methods – how to define outcomes, gather baselines, measure emotion, and link results to business or societal value. The WXO will keep surfacing tools and examples that prove what the community already knows: experience works.

Business & Capital: How to Find Funding & Meet Investors (16.3% of respondents)

Access to capital remains one of the biggest hurdles in the Experience Economy. Many strong ideas stall between pilot and permanence.

Founders and creators are asking for clearer routes to finance, investors who understand experiential models, and frameworks that show how experiences generate reliable returns – not just buzz.

Here are ten examples of what people told us:

- ‘Raising money, and finding locations for LBEs.’

- ‘Finding investment.’

- ‘Connect me to investors.’

- ‘Create a business plan that investors will understand.’

- ‘Develop the experience marketplace – draw a more direct line between experience and investment returns.’

- ‘We have proven‑concept IP and are searching for serious business‑minded partners for major expansion.’

- ‘Connect me to investors and like‑minded people who share our passion for immersive experiences.’

- ‘Developing the experience marketplace – draw a more direct line between experience and investment returns.’

- ‘How to show others that this way of “experiencing” art is valid… creating a business plan investors will understand.’

- ‘The need to develop a list of proven ways to measure experiences… for non‑believers and investors.’

What this means – and what we do next

Experience needs to be treated as an investable category – with clear models, measurable outcomes and credible paths to profit. Members are asking for investor education, case studies of successful funding rounds, and financial templates that translate creative language into business logic. The WXO will work to bridge this gap by connecting creators with capital and helping both sides speak the same language.

Impact & How to Design it: How to Change What People do, Know & Feel? (15.0% of respondents)

Experience professionals don’t just want to delight their audiences – they want to make a difference. They’re asking how to design experiences that shift behaviour, build understanding, and leave lasting emotional and social impact.

Here are eight examples of what people told us:

- ‘Help me see just how big and how impactful this work actually is in the world.’

- ‘How to create the best experiences for learning.’

- ‘Both promoting and discussing the social and cultural impact of physical spaces.’

- ‘How can design really create interpersonal and socio‑affective connections through customer experiences?’

- ‘How can we ensure experiential design transcends mere entertainment or gimmickry to deliver genuine added value?’

- ‘Helping our healthcare clients in rural communities understand the value in transforming their communities to thrive.’

- ‘Profile the most innovative travel experiences.’

- ‘Bring performance and practice that changes behaviour into the world.’

What this means – and what we do next

Impact is a chain: from attention to emotion to memory to behaviour. Members are asking for practical frameworks to design and measure that impact chain, with simple “do/know/feel” metrics that capture what truly changes over time.

Business & Expansion: How To Scale‑up & Expand (14.7% of respondents)

Growth takes many forms – replication, touring, franchising, entering new markets. Scaling is, of course, a different job from invention. Members want to know how to grow without diluting creative integrity or overextending operations.

Here are five examples of what people told us:

- ‘Staying relevant to audience expectations in a dynamic consumer landscape.’

- ‘How our company of world‑leading designers can scale while remaining agile and adaptable to such a diverse portfolio.’

- ‘We’re looking for major expansion.’

- ‘Help to bring the same degree of respect and legitimacy to the experience industry as exists for theme parks.’

- ‘Make immersive entertainment accessible for a broad audience.’

What this means – and what we do next

Simply put, studios want to scale without losing their soul. They’re asking for replicable business models, operational standards, local-supplier strategies and financial planning tools that support growth – but without sacrificing quality.

Sustainability: Shrink the Footprint, Not the Experience (12.6% of respondents)

Sustainability is now a design consideration, not a postscript. Members are focused on how experiences are made and run sustainably – think materials, energy, waste and travel – while keeping creative ambition high.

Here are seven examples of what people told us:

- ‘Create stunning experiences while also being mindful of our planet’s resources.’

- ‘How can we use cutting‑edge technology while staying cost and environmentally conscious?’

- ‘How to remediate the earth through experiences.’

- ‘Contributing to climate resilience through art and science.’

- ‘Access economically viable resources in order to create socially important experiences that make a positive change.’

- ‘Doing more for less – push the limits of creativity while supporting client budgets and environmental aims.’

- ‘How to build immersive worlds on a budget… with end‑of‑life in mind.’

What this means – and what we do next

Members want to move from principles to practice: carbon-lite sets, reusable systems, circular material planning, and transparent footprint reporting. The WXO will highlight proven examples where sustainability and creativity co-exist.

Constrained Craft: Premium Outcomes on Real Budgets (12.0% of respondents)

Budgets are shrinking, spaces are awkward, timelines are tight. For most teams, constraint isn’t a temporary setback – it’s the norm. The best creators are learning to turn limits into leverage.*

Here are ten examples of what people told us:

- ‘The brands today are expecting new creative ways to build experiences for their customers but their budgets are shrinking.’

- ‘Doing more for less. In a world of challenging budgets, how do we push the limits of creativity to deliver a great immersive customer experience within new constraints.’

- ‘How to give people the immersive experience they want with small budgets.’

- ‘Blending creativity with the right technologies to deliver innovative concepts and smart, budget‑conscious solutions by effectively integrating both low and high‑tech elements.’

- ‘Creating most awesome experiences with low budget.’

- ‘How to build immersive worlds on a budget for conferences, client centres, and sponsorship moments (Salesforce Dreamforce, IBM Think, etc.).’

- ‘How to advocate for budget spend internally.’

- ‘Balancing innovation with budget constraints.’

- ‘Access economically viable resources in order to create socially important experiences that make a positive change.’

- ‘Strengthening storytelling and traditional themed‑entertainment approaches to creativity in lower budget, impermanent and/or touring experiences.’

What this means – and what we do next

Constraint is universal. Members want proven design and production strategies that achieve impact without overspend – think streamlined workflows, re-use systems, and smarter material choices. WXO will surface these examples so others can apply them too.

*Note: This theme overlaps with Creativity & Craft (multi‑tag; totals exceed 100%). We’re naming it because the signal is strong and practical requests are consistent.

Get Clients & New Business (11.0% of respondents)

Beyond funding, many creators want steady pipelines, visibility and trusted routes to paid work. The challenge here is less about inspiration and more about conversion – how to package, pitch and sustain opportunity. Simply put, members want to turn great work into paid work.

Here are eight examples of what people told us:

- ‘Help us get exposure and clients for what we are building.’

- ‘Introduce me to people who appreciate my work and ideas that can expand it.’

- ‘Access opportunities to collaborate on new immersive experiences.’

- ‘Accessibility to studios/companies/creatives who want to create and open immersive destination experiences.’

- ‘Access to collaborative partners to mutually support and grow our businesses, teams and innovation.’

- ‘Providing greater access to entertainment professionals who are seriously business‑minded… we’re searching for the individuals/entities who will take this to the next level.’

- ‘Meet with people who have new and realised ideas.’

- ‘Give us exposure and clients.’

What this means – and what we do next

There’s demand among members for commercial enablement, not just inspiration: ways to reach buyers, package offers, build case assets, and repeat success. WXO will continue to connect members with clients, collaborators and platforms that turn ideas into income.

What does this mean for the WXO?

Ten priorities, stated plainly by the people doing the work.

Make digital behave in the room. Build belonging. Codify the craft. Design for impact (and prove it). Fund it. Scale it. Shrink the footprint. Turn constraints into an advantage. And enable commerce.

That’s the agenda for 2026.

Over the next year, the WXO will programme everything we do – our website content, our weekly Campfires, London Experience Week – around these tracks. We’ll favour shipped work over theory: working diagrams, budgets, and honest failures.

If you’re ready to show your working – and to share a template others can reuse – we want to hear from you.

Our method & data

We analysed open‑ended responses from 3,000+ WXO applicants. Because many entries touched multiple issues, percentages are multi-tag and exceed 100%.

- Designing for Impact counts audience‑change outcomes only (professional upskilling sits in Creativity & Craft).

- Sustainability refers to eco/operational footprint.

- Funding, Scale‑up and Constraint Craft are reported separately to reflect distinct asks.

If this sounds like your daily challenge, join the WXO – increase your chances of achieving your goals, and help raise the standard of experiences worldwide.